Watch the Lectures#

Paul Krugman - Predicting the World Economy

- Lecture 1 2019: The Calm Before the Storm

- Lecture 2 2020: The Pandemic

- Lecture 3 2021: Hope and Fear

- Lecture 4 2023: Post-Pandemic

- Lecture 5 The Ultimate Problem

Lecture 1: 2019 — The Calm Before the Storm#

Before examining the post-COVID world economy, we need to look at the situation right before COVID hit.

What was the world like before 2019? The film Parasite won awards, and there was the No Japan movement, among other things.

Before COVID, the world was at the peak of globalization. In terms of global output, the peak of world trade is hard to pin down exactly but is estimated to be around 2007. Then COVID brought everything to a halt.

Looking back at the past decade, one interesting fact is that technology was often disappointing.

When looking at total factor productivity, it's a measure of not "what is technology" but "what role does technology play."

2007 was an interesting year. From 2007, technology advancement slowed again, leading to a period of stagnating productivity. 2008 saw the global financial crisis, and it was also the year Apple first introduced the iPhone.

The 2000s weren't a great time for technology productivity. People hadn't quite figured out what to do with technology yet. They used it a lot for entertainment but didn't use it as much for managing actual productivity. The key point is that you can't judge the value of technology by "how cool and sleek it looks." Technology should be judged by "how much it can change the way people work."

Thermal power generation brought change. Internal combustion engines and electricity brought change too. But information technology, while necessary in our lives, hasn't changed all that much. Of course, there were other problems too — specifically, a shortage of productive workers.

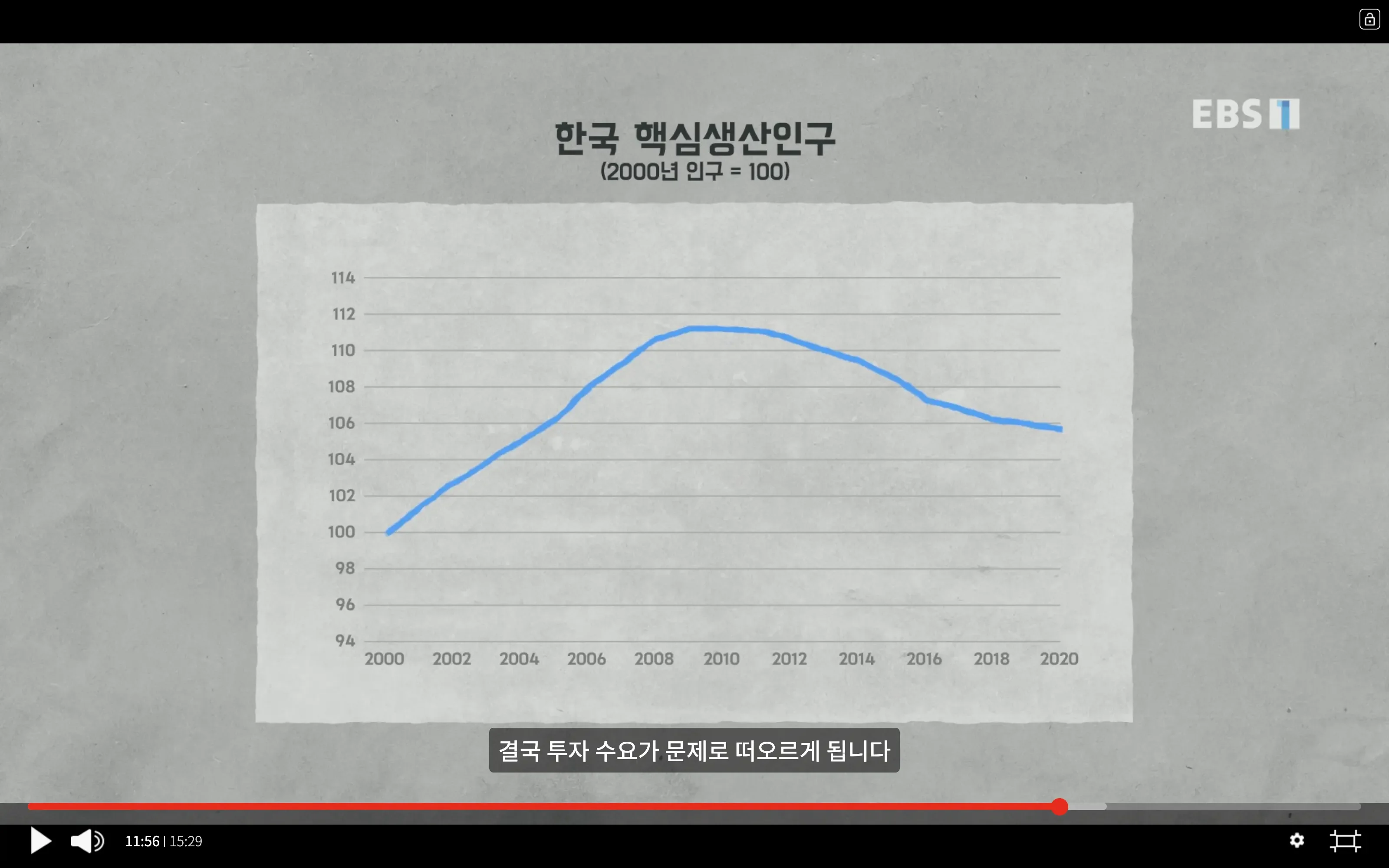

The core working-age population (typically ages 25-54) has been declining. Many countries are experiencing population decline. When population decreases, we do less harm to the environment because fewer resources are needed. What we need to do is build a good society even as the labor force keeps shrinking. The market economy matters to us. There needs to be sufficient demand in the private sector. We need to create new things that generate new demand. We need to get people spending rather than saving.

Korea's core working-age population has been declining for some time, and investment demand has become a problem. The industries that drove growth hit their limits, bringing crisis. The fact is that "these limits make us vulnerable."

Recessions appear like speed bumps you encounter while driving. No era is always good. Recessions always come back. On the road, shock absorbers help us pass safely. We rely on central banks, the Federal Reserve, the Bank of Japan, and the European Central Bank for that role. People expect each country's central bank to respond to downturns through interest rate cuts.

During COVID, we were completely unprepared for this kind of crisis. Economists expected things wouldn't be great, but nobody knew a catastrophic crisis was approaching.

Lecture 1 Summary#

Before the 2019 pandemic, the world economy had already reached its limits entering a "low-growth era"

3 obstacles to the world economy:

- Globalization stagnation due to declining production and purchasing: World trade relative to GDP decreased

- Declining technology productivity: New technologies failed to bring major change and didn't impact productivity improvement (total factor productivity decline)

- Declining core working-age population: Aging of core working-age generation (baby boomers) leading to insufficient replacement workforce

Total factor productivity: Worker productivity excluding capital factors

Core working years (Prime-working years): Ages 25-54 with high economic participation rates

Lecture 2: 2020 — The Pandemic#

Nobody predicted the COVID-19 pandemic. Accordingly, nobody anticipated the severe economic crisis that would follow.

Major international organizations and experts have never successfully predicted an economic crisis in advance.

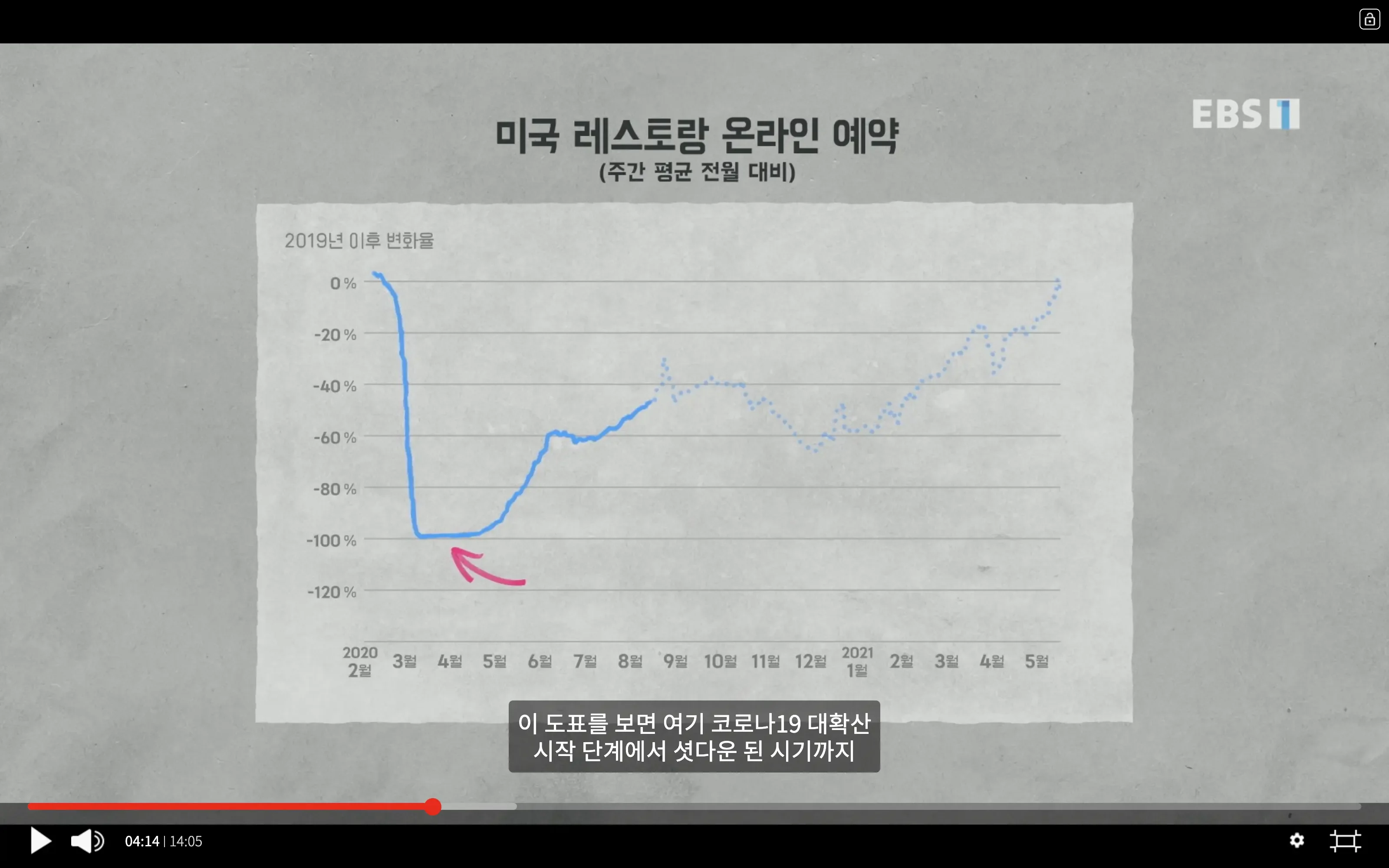

Everyone expected a vaccine would come, but it was certain it wouldn't arrive in time to prevent the disaster. So many major economies opted for shutdowns to prevent the spread of the disease. It was similar to a medically induced coma.

As a side note, the food service industry is part of the leisure and entertainment sector in modern affluent economies. It makes up a large part of the economy, which means disposable income is high. Jobs in this sector aren't essential for the world to keep running, but they make life enjoyable.

We actually handled COVID quite well. We responded appropriately to an unprecedented emergency. We came together and took action to get through a period of extreme hardship. But as shutdowns were implemented, people inevitably suffered negative aftereffects. The world economy was essentially on the verge of a serious financial disaster. A crisis severe enough to collapse the global financial system had arrived. If the financial system had collapsed, the suffering and disaster could have been even more devastating than the virus itself.

As the virus spread, everyone froze in fear of the future. Everyone thought, "I'm going to hold onto my cash. Lending is risky." This triggered a chain of financial crises, making the situation even worse. Fortunately, this crisis was very short — only about two weeks. It was resolved through massive capital injection. Institutions like the Federal Reserve and central banks poured in trillions of dollars.

Rather than letting the market fail, public institutions gave them a chance to be rescued with funds, and because public officials held to their duties even in extreme circumstances, we were able to overcome the financial crisis.

Lecture 2 Summary#

2020: Active responses from countries around the world -> Ending the pandemic crisis

- Economic coma — shutdowns to stop virus spread

- Massive government capital injection and asset purchases to calm the financial crisis

- Financial relief policies

- Disposable income (income individuals can freely spend or save after taxes) increased

- Savings grew due to income + relief payments + disrupted spending

Lecture 3: 2021 — Hope and Fear#

Will we really return to a world better than what we expected?

The worst of it caused enormous job losses. But recovery was happening quickly. The important question isn't "Will recovery be fast?" but rather "Is recovery happening too fast?" There's one more important question: "Are bottlenecks really the problem?" We may need to rethink inflation.

The economy is very complex. In the old days, producers manufactured goods and sold them to end consumers. But we live in a world of globalized production networks. If a link in the production chain breaks, it can affect places tens of thousands of kilometers away. A rapidly recovering economy can also bring severe price increases.

Lecture 3 Summary#

We're in an economic boom right now!

- Advances in biology -> Rapid vaccination expected to bring the worldwide virus under control

- End of pandemic emergency economic policies; liquidity provided in the latter half of the pandemic -> Potential help for future economic boom

The bottleneck problem (the dilemma of too-rapid economic recovery):

- Production capacity drops due to shortage of production factors

- Causes of bottlenecks

Overly expanded logistics systems from excessive globalization -> Labor shortage, supply can't meet suddenly recovered demand -> Pandemic inflation from rapid economic recovery => Price increases

Pandemic inflation -> A temporary transitional phenomenon

- Lumber supply increases leading to price drops, used car demand increases

- Core inflation vs. headline (short-term) inflation distinction

- Only lumber, used cars, and copper prices increased

- Expected return to pre-pandemic full employment

Lecture 4: 2023 — Post-Pandemic#

Lecturer Paul believes we can return to the pre-pandemic state. But there's something we need to think about. How much of the pre-pandemic problems remain? He views the stagnation of globalization and disappointing technological advancement as problems. It might be because these had already expanded to their maximum.

We could carry powerful computers in our pockets, but the expected economic growth never came.

We got real-world evidence that just because technology looks flashy and impressive doesn't mean it necessarily plays an efficient role in work.

In many ways, the world of 2023 is expected to be very similar to the world of 2019. However, there will be differences in how challenges and opportunities are presented. The pandemic will accelerate what was already happening and trigger significant new innovations.

Through this crisis, office workers experienced ways to work without going to the office. The interesting thing is that this was already technologically possible. In economics, there's a concept called "infant industry protection." It's used to protect domestic industries, but the pandemic showed an extreme example by forcing people to work from home.

What if business people didn't have to take long-distance business trips anymore?

If there's one thing lecturer Paul has learned over the past 15 years, it's that when faced with a truly serious crisis, modern society can come together in remarkably impressive ways.

Lecture 4 Summary#

The pandemic is both a new opportunity and a crisis

Pre-pandemic problems accelerated:

- Stagnation of globalization

- Low-productivity technology

- Declining working-age population (ages 20-64)

New innovations triggered by the pandemic:

- Collapse of existing work methods -> Remote work

- Opportunities for technology utilization

- Savings in commute and business trip time and resources

New crises from the pandemic:

- Collapse of existing work methods -> Collapse of facilities/real investment

- Decreased demand for commercial buildings -> Real estate crisis

- Non-performing loans, excessive bills, and other problems

Lecture 5: The Ultimate Problem#

There's something that must take priority over all other problems: climate change.

If you're not scared, you're probably not paying attention to climate change. Climate change is the most massive threat.

Actually, controlling climate change isn't impossibly difficult. The problem is that reaching political consensus before implementing anything is extremely, extremely difficult.

Economics says this: "Certain areas don't function properly without government intervention in the market." The most important of these is externalities — imposing costs on other people without any financial consequences.

The most serious negative externality is environmental pollution. We've seen countless cases of pollution that's invisible yet incredibly destructive. Climate change is completely different from a pandemic. Even if you tried to ignore the pandemic, you couldn't help but notice it. Climate change is about survival. It could mean the end of civilization.

Yet there are still so many people who don't believe in climate change. Some just don't want to believe that everyone should sacrifice for the common good.

Energy technology has far exceeded lecturer Paul's expectations. Wind power and solar power, which he once called foolish technologies, have become tremendously effective and cheap. The energy source that poses the greatest threat to climate change is coal-fired power.

We need to tax pollution emissions and introduce emission trading. But political implementation is extremely difficult. If you tell people you'll tax them for pollution from gasoline consumption, many drivers will be furious. Other policies can meet these requirements — like policies encouraging investment in green technology.

Technology is not only our friend, but it also tells us we don't need to do everything perfectly — what we have is good enough.

Economic nationalism is an obstacle to globalization, but it can also make political implementation more feasible. I believe we will solve this problem. Worries will continue, but I think the world of 2050 will be much better than we feared.

Lecture 5 Summary#

Climate change is on a different level from the pandemic

- A long-term future issue linked to the end of civilization

- The most massive threat humanity will face in 50 years, with no borders

Controlling climate change from an economic perspective:

- The simplest solution to serious externalities (environmental pollution) -> Economic sanctions

- Economic incentives -> Introducing pollution taxes, permit systems, emission trading rights, etc.

The miracle of technological progress: COVID-19 vaccines. Another miracle: affordable renewable energy technology

- Since 2008, energy technology has advanced making solar and wind power cheaper than coal

Controlling climate change from a political perspective:

- Push green technology investment incentive policies

- Green New Deal: Sustainable development policy centered on the environment and people

- Provide subsidies instead of taxes for clean energy and battery sectors

- Can be used as a means of job creation

- Government intervention in the market economy when needed -> Helps make political implementation more feasible

Controlling climate change from a global perspective:

- The U.S. leads by example -> Encourages Europe and Japan to follow

- Economic measures like carbon tariffs

- Imposing tariffs on exports from countries that reject climate change policies (international trade policy rules can be changed by WTO member agreement)

Climate change can be controlled, and the future in 50 years is optimistic

To hell with circumstances, I create opportunities.

— Bruce Lee